Discover how ADA compliance increases commercial property market value and tenant pools. Learn the hidden ROI of accessibility for savvy real estate investors.

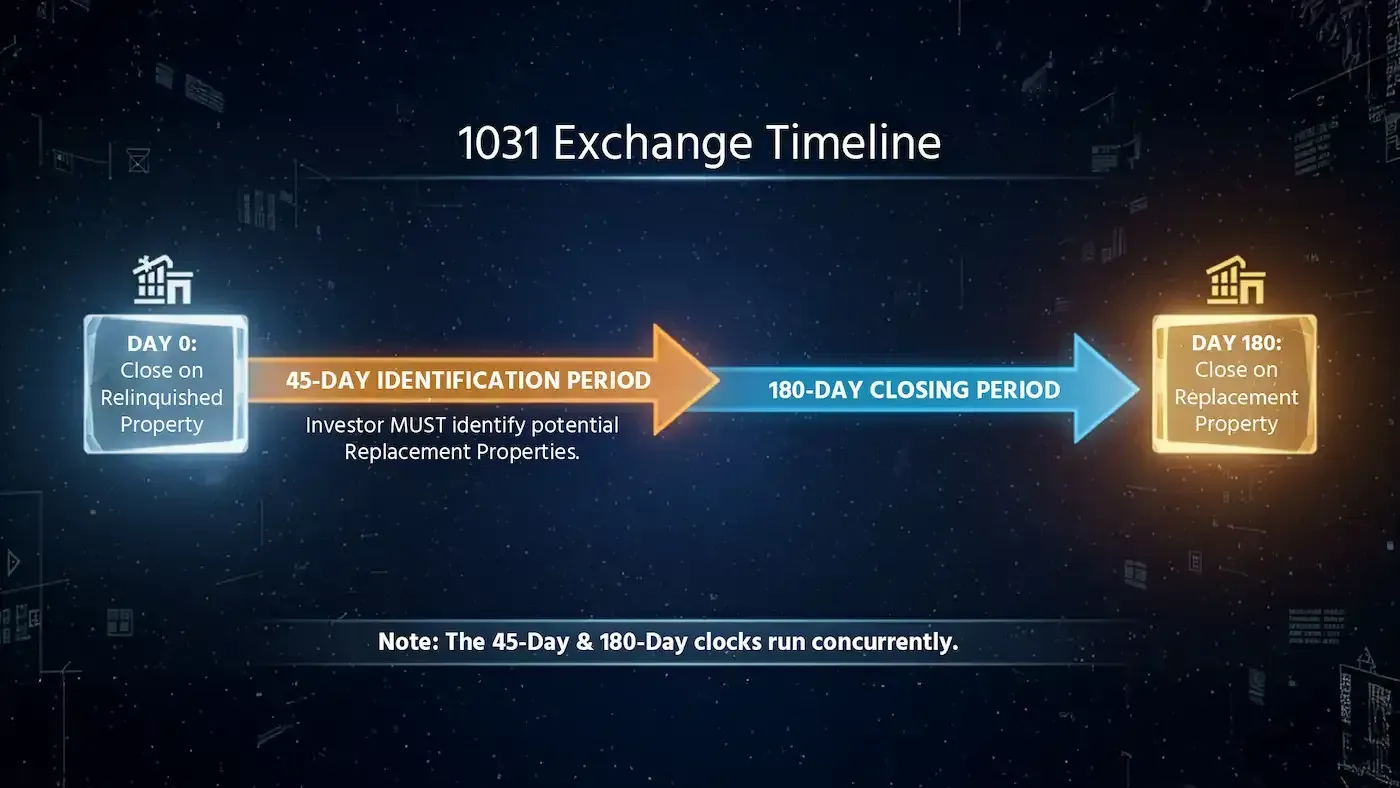

Master the 1031 exchange in Utah. Our complete guide covers the 45/180-day rules, like-kind property, and pitfalls to defer capital gains.

Falling commercial real estate interest rates in Utah create major opportunities. Learn how lower rates affect CRE property values, cap rates, and your buying power.